Tiger Global’s Lee Fixel is credited by many for partly shaping India’s internet economy, especially when it came to backing startups such as Flipkart early. Over the years, Fixel acquired dominance in large deals by aggressively chasing and wooing founders of some of India’s biggest technology companies including Sachin Bansal, Bhavish Agarwal and so on.

Even as Fixel played the role of a Godfather to the likes of Flipkart, he also encouraged entrepreneurs to cash out early, and start selling off their shares to build their wealth. By the time these companies would reach Series B or Series C funding rounds, the founders would have made multiples of their annual salaries in one secondary sale.

“He encouraged founders to cash out early so they achieve financial freedom and focus on building their startups without worrying too much,” said an entrepreneur who counts Tiger Global among its investors.

Other VCs too, started making investment offers to startups they really wanted, by bundling “secondary deals” in the term sheets.

At least four entrepreneurs I spoke with in the past two weeks confirmed that their term sheets had lucrative secondary sale of founder shares bundled in the contract.

“When you see how you can actually cash out few crores within months or a year of signing the term sheet, it’s tempting,” said one of them. “But then, you soon realise that it’s actually trading your control and freedom,” said one founder who has bootstrapped his startup over years.

Over years, this also bred a culture of entrepreneurs turning angel investors much before they established their own businesses. With financial freedom and early cash, why wouldn’t you write out small cheques of capital and become an angel investor in other startups, after all?

The frenzy to become an angel investor has reached a point where founders have even started pledging their shares to raise money from the banks. As one of the most respected and a veteran angel investor in India pointed out few months ago, some founders have even started defaulting on their promised angel investments because investors are now beginning to question secondary sales and are tightening their purse strings.

Over years, this also bred a culture of entrepreneurs turning angel investors much before they established their own businesses.

The question is, should the startup founders become angel investors even before their companies have reached a certain scale? And raising a Series A funding is not the scale I am talking about.

In fact, right after we announced FactorDaily’s first funding round, a bunch of investing platforms sent me emails asking “to participate in the Indian startup ecosystem by becoming an angel investor.”

Now, I am a rookie entrepreneur, learning and un-learning things all the time. It’s really difficult to imagine how just-born entrepreneurs like myself find time beyond establishing our own startups.

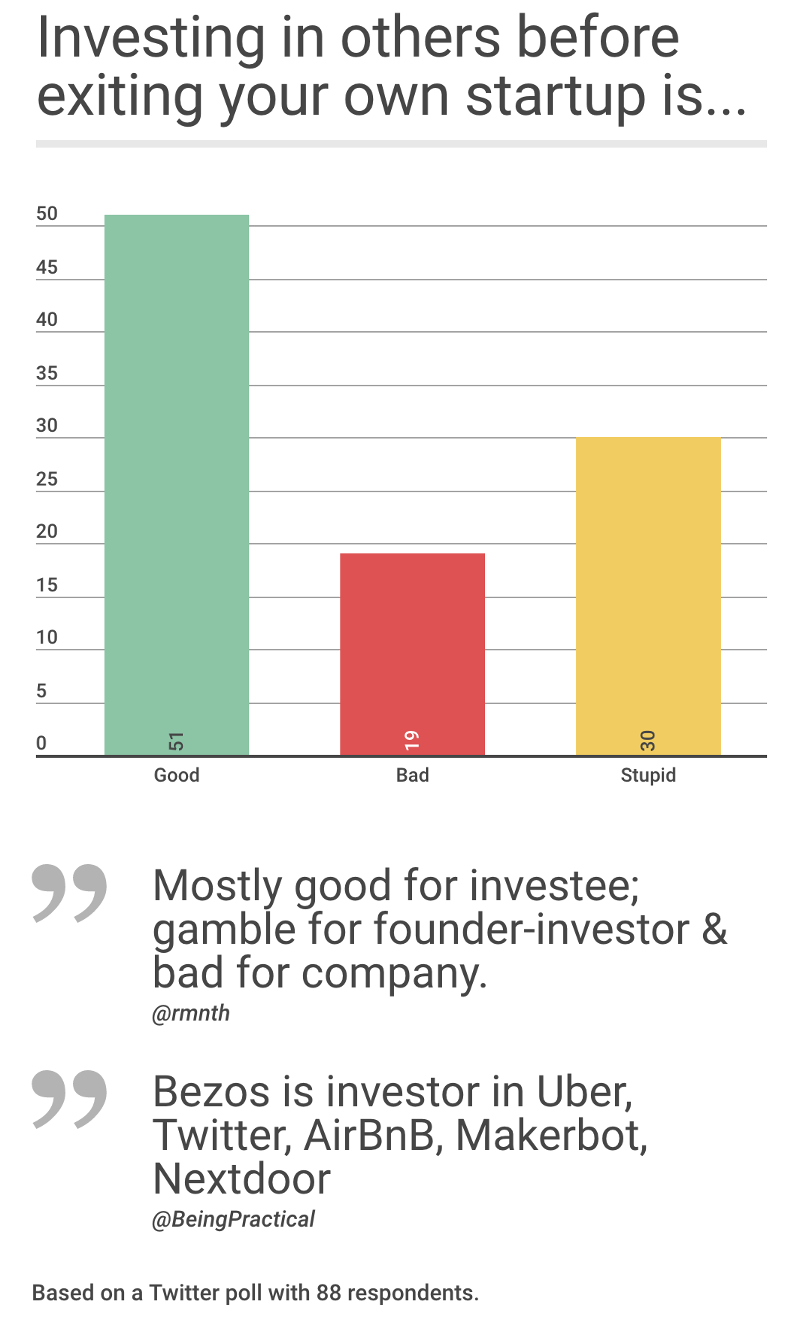

While we don’t have hard data to support the trend of Indian entrepreneurs cashing out early, my colleague Jayadevan PK ran a Twitter poll couple of weeks ago on the subject.

To be sure, Tiger Global and Fixel are not solely responsible for this trend of founders cashing out too much, too early. It’s a trend that became mainstream over past few years, possibly triggered by Fixel, but taken mainstream by several other investors. But now, the tides have turned and the focus is back on ruthless execution, unit economics and net promoter score– you know, the fundamentals of business that shouldn’t have been ignored in the first place.

For founders, it’s time to go back and focus on building their own companies. The glory and celebrity status of angel investing can wait, at least for now.

Subscribe to FactorDaily

Our daily brief keeps thousands of readers ahead of the curve. More signals, less noise.